Giovanni Serio, Vitol’s global head of research, recently presented our China medium term demand outlook at the FT Commodities Asia conference.

In the last 20 years China has been a primary driver of oil demand. From 2004 to 2024 Chinese oil demand has nearly tripled accounting for over half of oil demand growth globally.

Now that trend is being challenged.

Today, oil markets are asking whether Chinese oil demand, and particularly gasoline demand, has peaked, and what shape future Chinese oil demand will take.

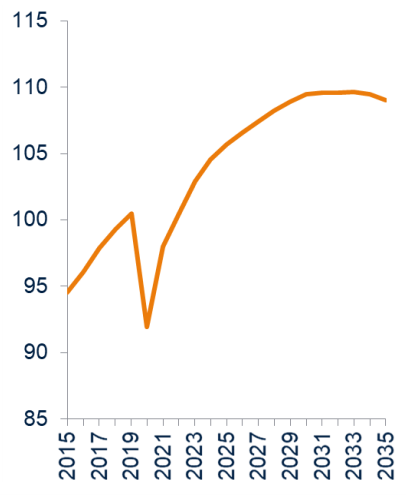

Global outlook

The trend of slowing popularity in EVs and lessening commitment to environmental targets is leading to a longer transition with global demand only peaking in the 2030s.

Future demand growth is almost entirely linked to petrochemical feedstocks – road fuels have already, or will soon peak.

Global demand outlook total liquids / mbpd

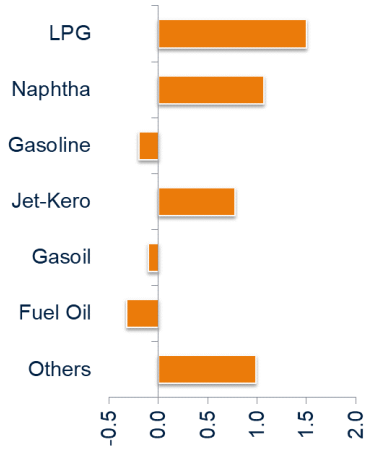

Product demand change 2023 basis /mbpd

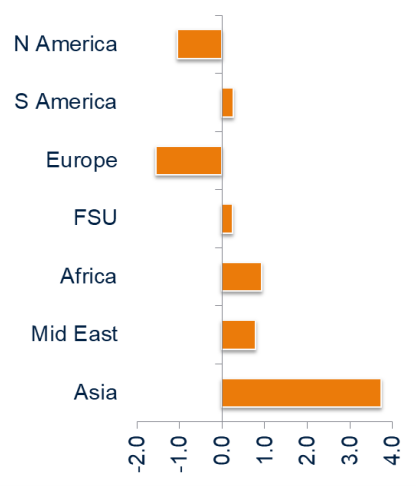

Regional outlook

The regional demand growth chart shows that Asia is the driving force of demand. Within the region, LPG, Naphtha and Jet continue to be the main drivers with a tapering road fuel demand.

Regional oil demand growth 2025-35 / mbpd

Asia oil demand growth 2025-30 / mbpd

China outlook

Oil demand trend and outlook

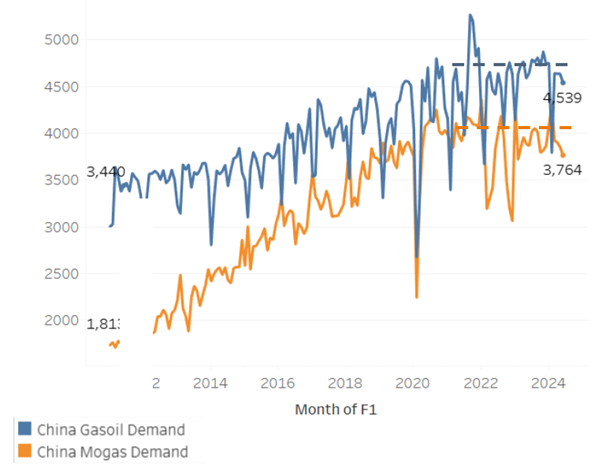

There has been a lot of focus in the last few months on the economic slow-down in China and the impact this might have on oil demand. Notwithstanding the headlines, the demand growth trend of imports + domestic crude production, looks similar to the slope before Covid.

It’s been weak in the last couple of months – but that is just volatility – the trend is the same. What has changed is the composition of that demand. It is very clear when you break it down that peak transport fuel has been reached in China, but that petchem continues to expand and drive demand growth.

China net supplies / kbpd

China demand trends / kbpd

Mogas and gasoil demand

Mogas and gasoil demand / kbpd

EV sales

Chinese policy has ensured that China’s EV penetration is higher than any other major market, with sales surpassing those of internal combustion engines for the first time this year.

One of the strongest drivers of this are plug-in hybrid electric vehicles (PHEVs), while battery electric vehicles (BEVs) have been growing but at a much slower pace. This is important because when you look at the outlook for oil demand you need to break it down by vehicle type – BEVs will not add to oil demand, while PHEVs will continue to drive some level of demand.

Other factors

Despite the high penetration of the electric fleet – particularly in the taxi and ride-hailing categories – there are some potential mitigating factors to the decline in gasoline demand. How these play out may have some impact on the overall trajectory that we’re seeing.

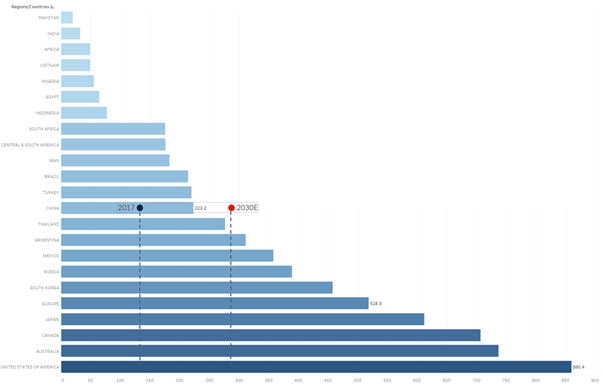

There has been a disconnect between the growth of the ICE fleet and gasoline demand. This is likely because car utilisation rates have not yet recovered to pre-pandemic levels in China, unlike most other countries. In addition, China has a per capita car ownership of 223.2 vehicles per thousand inhabitants, placing it between Turkey and Thailand. Should either of these factors materially change, (increased utilisation of ICE fleet, or increased ownership of ICE vehicles) then the demand outlook for gasoline may be affected.

But above all, two key factors stand out between bullish and bearish mogas – to what extent the current aging ICE fleet is renewed with EVs, and within that, what percentage of those are PHEVs.

Global car ownership rate (selected markets) / vehicles per 1,000 inhabitants

Gasoil demand medium term outlook

Largely drivers for gasoil demand are either linked to:

- the economy: like off-road consumption and total freight growth which is closely aligned to industrial production, or

- the energy transition: like road to waterway and railway freight. Freight accounts for 70% of total diesel demand. Heavy duty vehicle demand, which is most exposed to the switch to LNG, accounts for 40%.

LNG consumption – and therefore a reduction in gasoil demand – is entirely dependent on economics. Where LNG costs less, LNG truck sales rise and LNG consumption increases, and the reverse when diesel is less expensive. We’re forecasting poor LNG truck economics to 2027 and then a resumption of the LNG penetration trend once the economics make sense.

Global demand drivers going forward

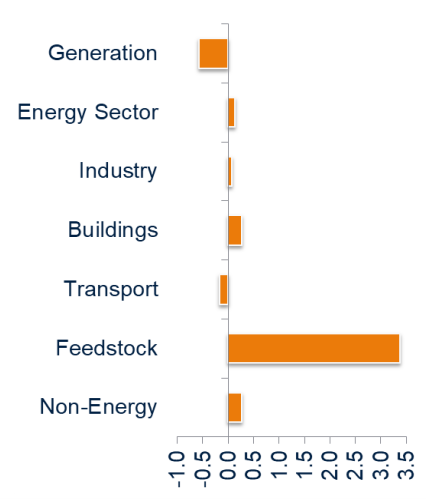

The big change globally, and evidenced here by China, will be that the driver of oil demand growth, will switch from transport fuels to petchem feedstock.

Global oil demand growth by sector 2025-30 / mbpd

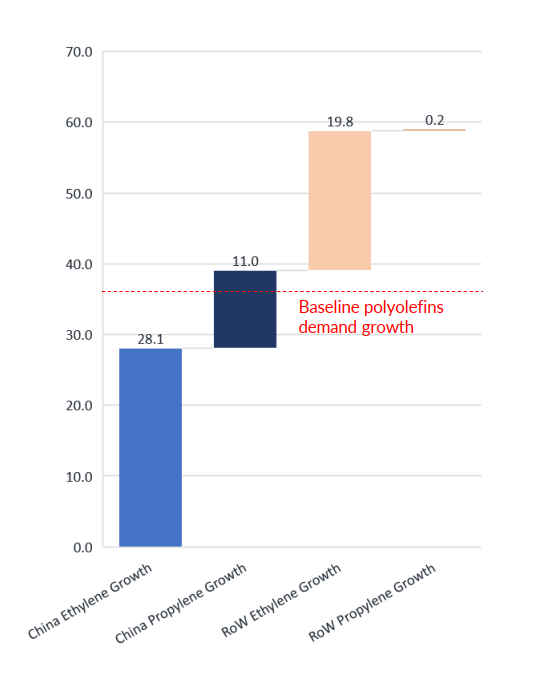

Olefins capacity growth, 2028 vs 2023 / mtpa

China is set to play a significant role with capacity increases in the next few years. The growth next year is entirely capable of satisfying the global plastic demand growth. And subsequent years will follow the same trajectory.

It is likely that petchem feedstocks will be the driving force of oil demand in China and globally.